The End of MAU—And Now MRR Can't Be Trusted Either

AI firms' 'annual revenue' is just monthly revenue × 12 — a fiction that breaks once inference costs hit margins directly.

This piece isn’t a blanket argument about all SaaS companies — it’s a critique focused specifically on AI businesses where inference costs feed directly into product cost and margin.

Opening

Hello, reader. This is Oswarld. Today I want to talk about something that leans a bit into GTM strategy territory.

This February, Anthropic announced its Series G funding round with a headline number: $14 billion in annualized recurring revenue (ARR). A $380 billion valuation. The label attached was “the fastest-growing B2B company in history.”

Yet just a month later, the company’s CFO, Krishna Rao, filed a sworn declaration with a U.S. court in a Department of Defense lawsuit — and it told a completely different story: “cumulative revenue to date exceeds $5 billion.” That’s everything the company has earned since it was founded, combined.

$14 billion versus $5 billion. Two numbers, from the same company, a month apart, from the same executive team. That gap is exactly what I want to unpack today. The tech industry’s “common metric” is once again on the verge of a generational shift.

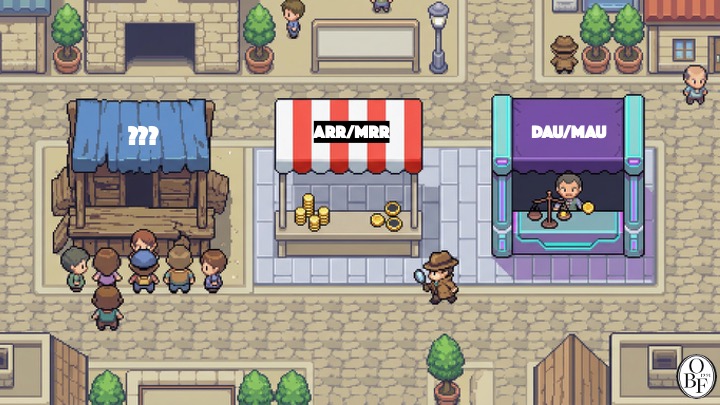

📐 A Brief History of Metrics: From DAU to ARR, and Back Again

Every era of tech has had a metric that everyone agreed you could “just look at this one number” to understand a company. And whenever that metric started diverging from reality, a new era began.

First generation: the DAU/MAU era (roughly 2007–2015). As smartphones and social media exploded, the industry was dominated by a single question: “How often do users come back?” Facebook, Twitter, and Instagram were valued by Daily Active Users (DAU)1 and Monthly Active Users (MAU). Investors watched these numbers, the press watched them, and executives watched them. The reasoning was simple. Back then, if you gathered users, ad revenue — or something — would follow.

But problems emerged. A service with 100 million DAU and another service with 100 million DAU could have wildly different business quality. Bot accounts got mixed in, the definition of “active” varied company to company, and more and more services had user counts that didn’t translate directly into revenue. DAU/MAU measured the scale of attention well, but it never showed the health of the business.

Second generation: the ARR/MRR era (roughly 2015–2024). As cloud computing and SaaS2 went mainstream, the industry’s question changed. “How predictably are you earning money?” Annual Recurring Revenue (ARR) — Monthly Recurring Revenue (MRR) multiplied by 12 — became the new common language.

ARR worked because of three characteristics of SaaS businesses. Gross margin3 ran high, at 80–90%. The marginal cost of serving one more customer was close to zero. And contracts really were “annual,” and really did “recur.” Under those three conditions, this month’s revenue × 12 came out almost equal to actual annual revenue. Boards understood it, CFOs could forecast with it, and investors could use it to compare companies. For fifteen years, nobody seriously questioned it — because there was no reason to.

And now, AI is breaking all three of these assumptions at once.

🔥 The Three Assumptions Behind ARR That AI Broke

Assumption 1: Marginal cost is nearly zero → Broken. In AI products, every single inference4 call is a real cost. Every time a user generates complex code or analyzes a long document, GPU costs land on the bill. According to tech journalist Ed Zitron’s reporting, Anthropic spent roughly $2.66 billion on AWS compute alone between January and September 2025, while its estimated revenue over the same period was about $2.55 billion. That means it spent more than 100% of its revenue on cloud costs.

Assumption 2: Cost differences between customers are negligible → Broken. Picture two customers, both paying $2,000 a month. Customer A runs light workloads and generates a 78% gross margin. Customer B runs massive, model-intensive tasks every day and generates a 31% gross margin. On the ARR dashboard, both show up identically as $24,000 a year. There’s no way for ARR to reveal that Customer B is quietly wrecking the unit economics5. The top 5% of customers consuming 75% of total compute costs while paying the same flat rate as everyone else — that’s simply the default state of flat-rate AI products.

Assumption 3: “Recurring” is guaranteed → Shaky. In SaaS, switching costs were high — data migration, employee retraining, workflow redesign, the whole ordeal. But switching AI tools can take a few hours. You just swap an API key. The very premise of “Recurring” is an optimistic one. That said, this doesn’t apply equally to every AI product. Products deeply embedded in workflows and data still carry high switching costs. But for API-centric or abstracted usage layers, switching friction can end up far lower than in SaaS.

Once all three assumptions start to wobble, ARR becomes a metric that’s hard to interpret on its own — especially for businesses where AI inference costs feed directly into cost of goods sold. It’s the same structural failure as the moment DAU stopped explaining business quality. Have you noticed the words “growth marketing” and “performance marketing” showing up less lately? As those three assumptions crumbled, the playbook that ruled the first and second generations simply stopped working. A new grammar is now needed.

📊 Behind the Numbers: Anthropic and OpenAI

The two most-watched AI companies right now are proving this isn’t just an abstract argument.

Anthropic announced ARR starting at $1 billion in December 2024, then $4 billion in July 2025, $9 billion in December, and $14 billion in February 2026 — a tenfold increase in fourteen months, a pace no B2B software company has ever hit before in history. Yet on March 9 of that same year, the CFO’s sworn declaration to a U.S. court stated cumulative revenue since founding “exceeds $5 billion.” Ed Zitron worked backward from Anthropic’s announced ARR figures to estimate cumulative revenue, and arrived at at least $6.66 billion — a number that lines up with neither the $5 billion figure nor the $14 billion figure. On top of that, the money spent on inference and training exceeded $10 billion.

OpenAI shows the same pattern. CFO Sarah Friar announced in January 2026 that “2025 ARR exceeded $20 billion.” But according to first-half results disclosed in September 2025, actual revenue for the first half was about $4.3 billion, with cash burn of $2.5 billion — putting the company on an annualized revenue pace of roughly $13 billion, a considerable distance from the $20 billion ARR figure.

Just as the definition of “active user” varied from company to company in the DAU/MAU era, in the ARR era the word “annualized” is being used with a meaning that diverges from actual annual performance. And that gap is measured in billions of dollars. In other words, it’s not that the concept of recurring revenue is disappearing — it’s that recurring revenue alone has become insufficient to explain the quality of a business.

🔄 Candidates for the Third-Generation Metric

So what comes after ARR — what will be the common language of the AI era? There’s no consensus answer yet, but two candidates are emerging as frontrunners in the industry.

First, Productivity per Dollar Spent. In the SaaS era, “ARR ÷ headcount” was the go-to metric for measuring company efficiency, because employees were the main cost. But if an AI agent is handling a workflow equivalent to 40 hours a week, that’s not a software subscription — that’s a labor cost.

GTM strategist Kyle Poyar’s proposal is clear-cut: include AI agent costs in the denominator alongside labor costs, making it ‘ARR ÷ (labor cost + AI spend).’ Some companies that ran this calculation for the first time discovered that an efficiency metric that looked perfectly healthy under the old “ARR ÷ headcount” formula had actually been declining for two straight years.

Venture capitalist Tomasz Tunguz went a step further, analyzing gross profit per token across six AI companies. The results are striking: the correlation between gross profit per token and valuation was 0.70, while the correlation between raw token throughput and valuation was only 0.47. That means investors are already looking not at “how much” but at “how much is left over.”

Second, First Year Value. In SaaS, the LTV/CAC6 ratio was the core metric of investment efficiency. It’s the ratio of customer lifetime value divided by customer acquisition cost. But former CFO CJ Gustafson says applying this to AI startups is closer to “a numbers game.”

The reason is simple. Nobody knows how long an AI customer’s “lifetime” actually is. Switching friction is lower than for any software in history, and a tool that replaces yours can be deployed in a matter of hours. LTV assumes low churn, predictable expansion, and long retention — and AI products haven’t proven any of these three yet.

First Year Value asks a sharper question: “Did this customer get enough value in the first 12 months to justify renewal?” If the answer only becomes ‘yes’ in year two or three, then a good-looking LTV is actually masking a retention problem.

Oz’s Lens

Looking back at these generational shifts in metrics, a pattern emerges. A metric is the shadow of a business model. When the ad model dominates, DAU/MAU reigns; when the subscription model dominates, ARR reigns. And when the business model changes but the metric doesn’t, that gap creates a multi-billion-dollar illusion.

In my own experience building GTM strategy, a metric is never just a measurement tool — it’s an incentive structure that shapes organizational behavior. A sales team at a company that uses ARR as its KPI optimizes for the size of revenue, not for profitability per customer. Anthropic announcing $14 billion in ARR and being awarded a $380 billion valuation is a textbook example of how this structure plays out.

But I don’t think this structure can last much longer. We’re living in an era where cumulative revenue gets exposed in court declarations, and independent journalists track and report AWS spending. The makeup covering ARR is coming off faster and faster. Founders, consumers, and investors are all getting sharper. That also means the era of playing games with metrics is coming to an end.

- Adding AI to a business doesn’t automatically make ARR meaningless everywhere. But the story changes for models where AI inference costs feed directly into cost of goods sold, margin variance widens based on per-customer usage intensity, and — in some areas — switching friction drops as well. In these cases, ARR remains an important growth metric, but on its own it becomes insufficient to explain the quality of the business. What I want to say isn’t that ARR should be discarded, but that the AI era needs a new interpretive framework that reads cost structure and retention structure alongside ARR.

But to be honest, the biggest bottleneck for new metrics isn’t awareness — it’s infrastructure. Tracking gross profit per token per customer in real time requires connecting the billing system, infrastructure cost reports, and finance team spreadsheets into a single pipeline. At most AI companies, these three systems don’t talk to each other. Adopting third-generation metrics ultimately comes down to a billing architecture problem too.

Closing Thoughts

To sum up: just as DAU/MAU was the language of the ad model and ARR was the language of the subscription model — the AI era needs a new language that reflects cost structure. Productivity per dollar spent and First Year Value are the first drafts of that language.

If you’re investing in AI companies, adopting AI products, or running an AI business — ask about gross profit, not revenue; ask what’s left after the first year, not the growth rate. This is the moment to develop an eye for reading the structure of numbers, not just their size.

References & Further Reading

- Ed Zitron, “Why Are We Still Doing This?”, Where’s Your Ed At, March 17, 2026. : An analysis that works backward through the gap between Anthropic’s ARR announcements and its court declaration figures.

- Ed Zitron, “How Much Money Do OpenAI And Anthropic Actually Make?”, Where’s Your Ed At, October 17, 2025. : An analysis that works backward through the gap between Anthropic’s ARR announcements and its court declaration figures.

- Tomasz Tunguz, “Gross Profit per Token”, December 30, 2025. : An analysis of the correlation between gross profit per token and valuation across six AI companies — showing with data what investors are actually looking at.

- Shanaka Anslem Perera, “The Growth Miracle and the Six Fractures: Anthropic at $380 Billion”, Substack, February 18, 2026. : An in-depth analysis of six structural risks lurking behind Anthropic’s growth narrative.

- Kyle Poyar & CJ Gustafson, Mostly Growth podcast. : A podcast that takes a practical look at monetization strategy and metrics for SaaS/AI companies, digging into topics like productivity per dollar spent and the limits of LTV.

The author, Kwangseob Ahn, is a professor of business administration at Sejong University and lead consultant at OBF (Oswarld Boutique Consulting Firm). He teaches statistics and data analysis — business data management and business analytics — while leading GTM and AI strategy consulting in the field, designing the seam between technology and business. He has published academic research on a memory architecture for AI dialogue systems (HEMA) and runs Daily Arxiv, a daily curation of global AI papers. He holds a master’s from Korea University’s Graduate School of Technology Management and a KMBA. He is the author of Homo Brainless: The People Who Outsource Their Thinking.

Footnotes

-

DAU/MAU (Daily/Monthly Active Users): the number of people who actually used a service within a day or a month. This was the core metric of the early-2010s social media and mobile app era. Its limitation was that the definition of “active” varied by company, making comparisons difficult. ↩

-

SaaS (Software as a Service): a model where software is used via subscription in the cloud rather than installed locally. Slack, Notion, and Salesforce are representative examples. ↩

-

Gross Margin: the ratio of revenue remaining after subtracting direct costs (cost of goods sold). If you earn 100 won and it costs 20 won to deliver the service, that’s an 80% margin. In SaaS, 80–90% was typical, but at AI companies it often drops to the 40–60% range. ↩

-

Inference: the process by which an already-trained AI model actually generates a response. Training is the process of building the model; inference is the process of using the built model. Most of an AI service’s operating cost comes from here. ↩

-

Unit Economics: an analysis of profitability on a per-customer or per-transaction basis. Even if total revenue grows, if each individual customer is unprofitable, it shows a structure where losses grow larger as the business scales. ↩

-

LTV/CAC ratio: the ratio of Lifetime Value to Customer Acquisition Cost. A ratio of 3x or higher is typically considered healthy. In the AI era, this metric is losing reliability because “lifetime” has become hard to predict. ↩

Your take shapes the next issue

Reply with your experience or perspective — the best responses feed into future issues.

Sign in to comment Any registered reader can comment — it takes 10 seconds.