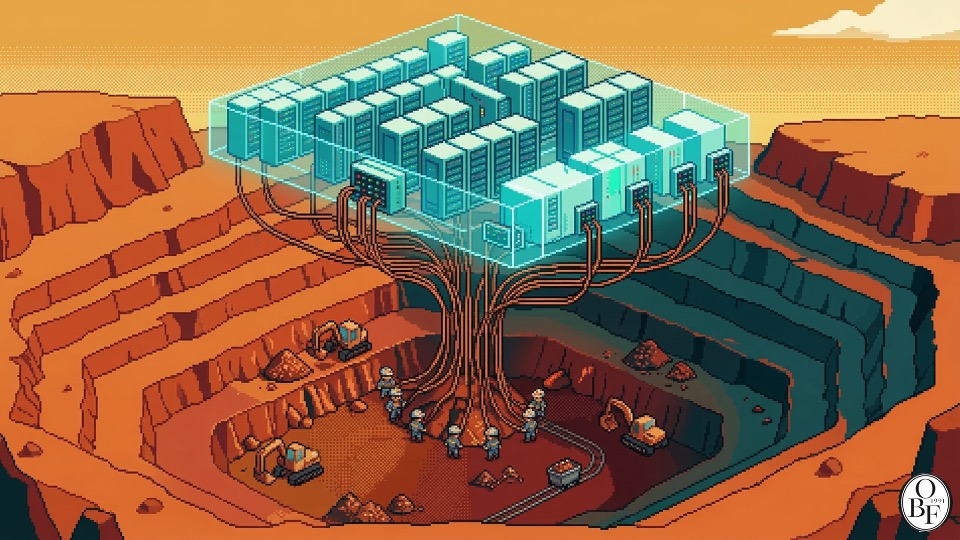

Why "Software Eats the World" Has Expired

As AI makes software abundant, economic power is swinging back toward the physical world of hardware.

Opening

Dear subscriber, there’s a sentence Marc Andreessen wrote in a 2011 Wall Street Journal op-ed. “Software is eating the world.” For the 14 years since, that line has functioned as something like an axiom in Silicon Valley. Netflix devoured Blockbuster, Uber swallowed the taxi industry, Airbnb consumed the hotel business. Competitive advantage lived in code, not in physical assets.

But a fascinating column recently ran in The Economist. Written by Paul Achleitner, the former chairman of Deutsche Bank’s supervisory board, its core argument is this: AI has turned software into a commodity1, and as a result, economic power is migrating back toward hardware — energy, minerals, infrastructure, manufacturing capacity. Today let’s examine whether this claim actually holds up, and what it means for us.

Why Software Stopped Being a “Scarce Resource”

The reason Andreessen’s 2011 thesis worked is clear. The capacity to build software was itself scarce. Only companies that could secure skilled developers and had the infrastructure to deploy code at scale survived the competition.

AI is flipping this arrangement. The cost of generating, testing, and optimizing code has started converging toward zero. That’s the context behind the term “vibe coding.” If software was once a “strategic asset” like oil, it’s now becoming closer to something “taken for granted,” like electricity.

A basic economic principle is at work here. Economic power attaches not to the most elegant thing, but to the scarcest thing. As software has become abundant, hardware’s constraints are coming back into focus.

Energy: The Physical Footprint of the Digital World

This shift is most visible in energy. The terawatt-hour (TWh)2 is becoming the standard unit of discussion. According to the IEA’s (International Energy Agency) special report from April 2025, global data center electricity consumption is projected to more than double from roughly 415 TWh in 2024 to 945 TWh by 2030. That’s roughly equivalent to Japan’s entire annual electricity consumption. AI is the single largest driver of this growth, with power demand from AI-optimized data centers expected to more than quadruple over the same period.

Here’s a striking figure. By 2030, U.S. data centers are projected to consume more electricity than all of the country’s energy-intensive manufacturing sectors combined — aluminum, steel, cement, chemicals, everything. The electricity used to process data will exceed the electricity used to make physical things.

The problem is that the infrastructure to supply this doesn’t exist yet. The IEA warns that roughly 20% of planned data center projects could be delayed due to grid connection bottlenecks. Building a single new transmission line takes 4 to 8 years in advanced economies. Software can be reshored3 in a matter of months; power plants and transmission grids cannot.

Copper: The Real Bottleneck of the Electrification Era

After energy comes materials. And among materials, copper is the linchpin.

According to a January 2026 report from S&P Global, “Copper in the Age of AI,” global copper demand is projected to grow 50%, from roughly 28 million tons today to 42 million tons by 2040. Rising demand is one thing, but the real problem is supply. Ore grades4 at existing mines are declining, and it takes an average of 17 years to take a new mine from discovery to production. The report projects a supply shortfall of roughly 10 million tons by 2040.

Copper matters for a simple reason: wherever electricity flows, copper has to be there too. Data centers, electric vehicles (which use 2.9 times more copper than internal combustion vehicles), solar and wind farms, transmission and distribution grids, even military equipment. S&P Global Vice Chairman Daniel Yergin put it this way: “Copper is a key enabler of electrification, but the very acceleration of electrification is becoming a challenge for copper.”

Software never had this kind of bottleneck. There’s essentially no marginal cost5 to copying code. But to mine one more ton of copper, you have to dig it out of the ground, refine it, and transport it. The fact that physical resources carry marginal costs — forgotten during the software era — is a basic economic principle resurfacing.

Processing: The Real Chokepoint Isn’t the Mine, It’s the Refinery

There’s a passage in Achleitner’s column that caught my attention more than any other. “Mining is only part of the story. Processing is the real chokepoint6 — the most geographically concentrated part of the supply chain.”

Rare earth elements7 make this vivid. China accounts for roughly 60-70% of global rare earth mining, but about 90% of refining and processing. That figure climbs to 94% once you get to permanent magnet manufacturing. According to the IEA’s 2025 report, China is the largest refiner in 19 out of 20 strategically important minerals, with an average market share of 70%.

In 2025, China actually played this card. In April, it began export controls on seven heavy rare earth elements; in October, it extended those controls to refining technology, equipment, and components. It even introduced extraterritorial jurisdiction8 requiring export licenses for products made overseas using Chinese technology.

This isn’t a simple trade dispute. China has understood for decades that processing capacity is strategic autonomy itself. Software can be shared as open source, but refining know-how and supply chains can’t be copied.

Oz’s Lens

Honestly, when I first read this column, my initial reaction was “another hardware renaissance story?” This kind of argument has come up before — during the semiconductor shortage, during the pandemic supply chain crisis.

But this time feels a bit different. The premise here is that AI is structurally dismantling software’s scarcity. If the earlier “hardware matters again” arguments were reactions to temporary supply shocks, this discussion is about a shift in the center of gravity of economic power.

There’s a pattern I’ve noticed. The moment tech companies define their identity as “we are a software company,” they start underestimating physical constraints. We call it the cloud, but its substance is server farms sitting on land. We call it AI, but its substance is GPU clusters devouring electricity. The phrase “weightless digital economy” was close to a misconception from the start.

That said, we need balance here. Software becoming a commodity doesn’t mean software has stopped mattering — just as electricity is a commodity, yet nothing works without it. It would be more accurate to say software’s role is shifting from “differentiator” to “essential infrastructure.” And the axis of competition is moving from “who writes better code” to “who can build and secure more stable physical systems.”

Viewed from the Korean context, this shift is also an opportunity. Korea, Taiwan, and Japan hold a global lead in the physical capability of semiconductor manufacturing. This capability rests on decades of accumulated engineering know-how — it’s not something that can be caught up to in a few months, the way software can. The question is whether this advantage can be extended into materials, energy, and processing.

Closing

To summarize: First, as AI makes software abundant, the axis of economic scarcity is shifting from the digital to the physical realm. Second, energy, materials, and processing capacity are likely to become the core variables determining competitiveness over the next decade. Third, in this transition, the advantage goes not to those with rapid scalability, but to those with long-term capital, engineering depth, and supply chain resilience.

Next time you hear the phrase “the AI era,” I’d suggest picturing not the code itself, but the physical foundation that code runs on. Without copper wire laid in the ground, neither AI nor electricity flows.

References & Further Reading

- Paul Achleitner, “Economic power is returning to the physical realm”, The Economist, 2025. : The column that sparked today’s newsletter. It systematically develops the thesis that “hardware is eating software.”

- IEA, Energy and AI (Special Report), April 2025. : The most comprehensive global analysis of data center power demand forecasts. The original source of the 945 TWh projection for 2030.

- S&P Global, Copper in the Age of AI: The Challenges of Electrification, January 2026. : The original source for the 50% increase in copper demand and the projected 10 million ton supply shortfall. Daniel Yergin co-chaired this report.

- Marc Andreessen, “Why Software Is Eating the World”, The Wall Street Journal, August 20, 2011. : The original thesis today’s newsletter is “rebutting.” Reading it again 14 years later reveals its blind spots.

- IEA, Global Critical Minerals Outlook 2025. : Contains data on China’s concentration in critical mineral refining (ranked #1 in 19 of 20 strategic minerals, with an average 70% market share).

- CSIS, “Developing Rare Earth Processing Hubs: An Analytical Approach”, July 2025. : An analysis of the rare earth processing hub potential of the U.S., Australia, Saudi Arabia, and Canada. Useful for understanding why breaking dependence on China is so difficult.

The author, Kwangseob Ahn, is a professor of business administration at Sejong University and lead consultant at OBF (Oswarld Boutique Consulting Firm). He teaches statistics and data analysis — business data management and business analytics — while leading GTM and AI strategy consulting in the field, designing the seam between technology and business. He has published academic research on a memory architecture for AI dialogue systems (HEMA) and runs Daily Arxiv, a daily curation of global AI papers. He holds a master’s from Korea University’s Graduate School of Technology Management and a KMBA. He is the author of Homo Brainless: The People Who Outsource Their Thinking.

Footnotes

-

A commodity is a good where quality barely differs regardless of who makes it, so competition happens purely on price. Wheat and crude oil are classic commodities — and this column’s core argument is that AI is pushing software in that same direction. ↩

-

A unit of electricity consumption. 1 TWh is roughly the amount of power 1 million households use in a year. 945 TWh is more than 1.5 times Korea’s entire annual electricity consumption (roughly 600 TWh). ↩

-

Reshoring: bringing production facilities or business functions that had moved overseas back to one’s home country. Software can be “reshored” remotely and quickly, but reshoring manufacturing takes years. ↩

-

Ore Grade: the proportion of metal that can actually be extracted from mined ore. The higher the grade, the more metal you get from the same amount of earth. Average ore grades at copper mines worldwide are declining, meaning it now costs more money and energy to obtain the same amount of copper. ↩

-

Marginal Cost: the additional cost of producing one more unit of a product or service. Copying software has a marginal cost near zero, but mining one more ton of copper adds costs for extraction, refining, and transport. ↩

-

Choke Point: a bottleneck point where flow narrows in a supply chain. Originally a military term for geopolitically critical passages like the Strait of Hormuz, here it’s used as a metaphor for processing and refining capacity concentrated in a single country. ↩

-

Rare Earth Elements: a collective term for 17 elements including lanthanum and neodymium. They are essential materials for EV motors, wind turbines, and precision-guided weapons — and since refining and processing are far more concentrated than mining, their strategic importance is even greater. ↩

-

Extraterritorial Jurisdiction: applying legal regulations to activities occurring outside one’s own territory. The rule China introduced in 2025 requires export licenses even for rare earth products made overseas using Chinese technology — meaning China seeks to control the use of its technology even abroad. ↩

Your take shapes the next issue

Reply with your experience or perspective — the best responses feed into future issues.

Sign in to comment Any registered reader can comment — it takes 10 seconds.