SpaceX at $135: Dream Price or Bubble Price?

Institutions bid 4x the offering while Morningstar says $63 — the gap is a bet on data centers that don't exist yet.

Opening

Dear readers, tomorrow (June 12) the most expensive name in history joins the Nasdaq: SpaceX. The IPO price is $135 per share, for a valuation of $1.75 trillion — roughly ₩2,400 trillion in Korean won. Early this morning, SpaceX even held a public webinar fronted by its CFO and COO.

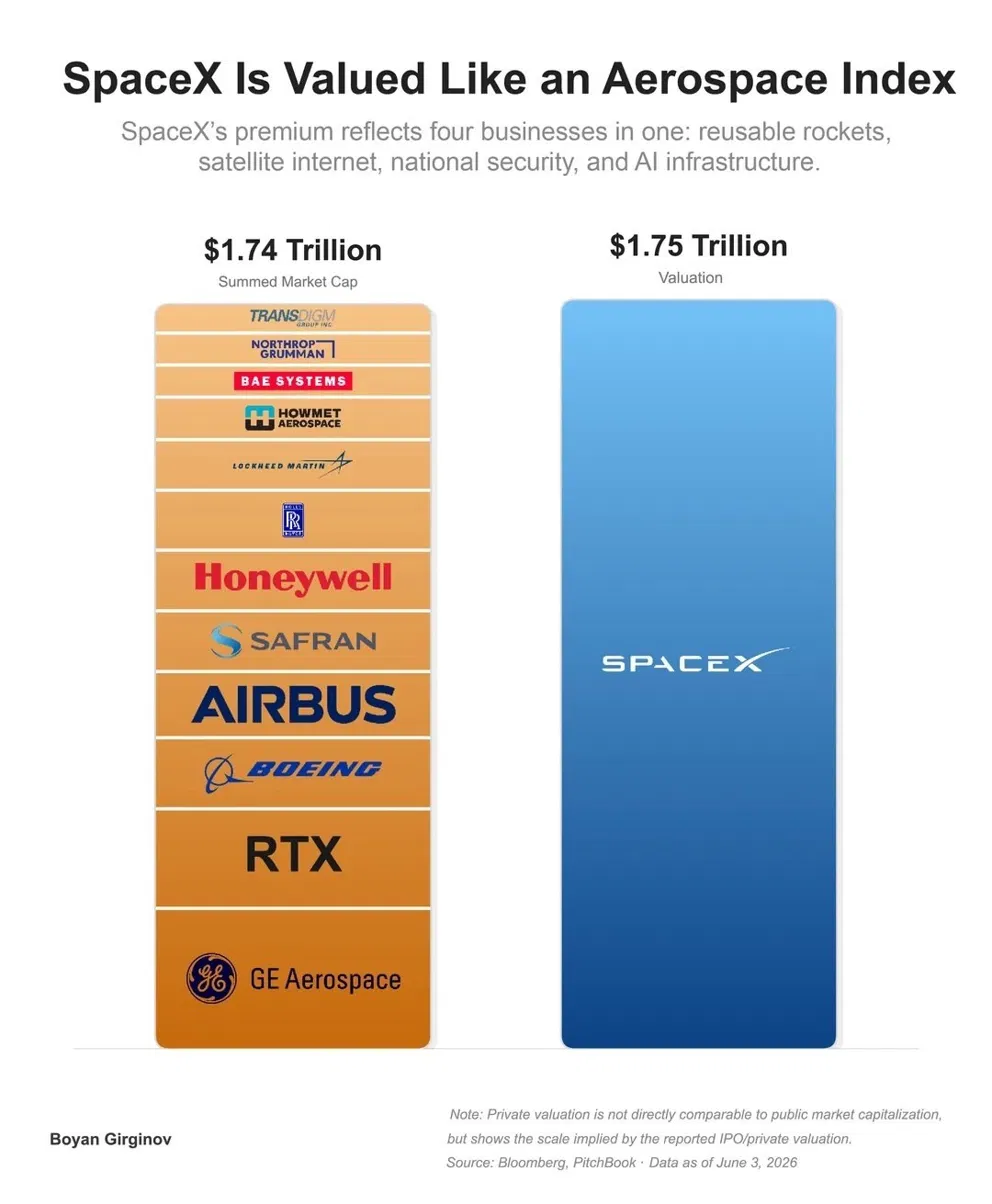

It can be hard to grasp how large that number is. So here’s one comparison. Boeing, Airbus, Lockheed Martin, RTX, Northrop Grumman, GE Aerospace… add up the market caps of the world’s 12 major aerospace companies and you get $1.74 trillion. Almost exactly the price of SpaceX alone.

Institutional investors brought in $250 billion of subscription demand — more than 4x the amount on offer. Morningstar, meanwhile, flatly declared that fair value is $63, less than half the IPO price. It is rare to see judgments split this extremely over the same company.

Let me give you the conclusion up front. The decisive variable in this IPO is not the rockets, and it is not Starlink. It is the value of an imagined business called the ‘AI data center’ — one that has yet to reach orbit.

The Numbers History Will Record

SpaceX’s IPO is rewriting the record books on every dimension.

Start with the size of the raise. SpaceX plans to sell 555.6 million shares to raise about $75 billion. That is more than 2.5x the previous all-time record IPO, Saudi Aramco in 2019 ($29 billion). On listing, its market cap will vault straight into the world’s top 5, behind Apple, Nvidia, Microsoft, and Amazon. The ticker is SPCX.

There are three structural anomalies worth watching.

First, the retail allocation is 30%. In a typical IPO, individual investors get 5–10% of the shares. This triples that. Elon Musk, who understands the loyalty of the Tesla shareholder community better than anyone, can be seen as deliberately engineering the conversion of retail ‘fandom’ into IPO demand.

Second, Nasdaq changed its rules. Previously a company had to wait months after listing to join the Nasdaq-100 index; under the new rule, SpaceX can enter the Nasdaq-100 just 15 days after listing. ETFs and funds tracking the index will have to buy SpaceX shares automatically, creating what amounts to ‘forced buying’ demand right after the debut.

Third, the gap between insider and outside-investor cost basis is extreme. Early investors and employees acquired their shares at an average of about $6.5 per share. That is roughly 1/20th of the $135 retail investors will pay. Musk has pledged not to sell his stake (about 42%) for 1 year after listing, but the lock-up expiry dates for other insiders deserve close attention.

Inside the $1.75 Trillion

Let’s break down exactly where this astronomical value comes from.

According to SpaceX’s S-1 filing1, the business splits into three main pillars. The merger with AI company xAI this February reshaped the company’s structure significantly. Based on 2025 revenue of $18.7 billion, it looks like this.

- Starlink (satellite internet): revenue of $11.4 billion, 61% of the total. This is the company’s real profit engine. It posted operating income of $4.4 billion, up 120% year over year. As of June 5, global subscribers surpassed 12 million, growing by about 1 million every month. Starting this May it began raising monthly subscription fees by up to $10 — a signal that it has moved past the subscriber-acquisition phase into monetization.

- Launch services (Space): revenue of $4 billion, 21% of the total. Falcon 9 completed 165 launches in 2025 alone, holding roughly 90% of global orbital launches. But growth was just 8%. Three-quarters of all launches carry the company’s own Starlink satellites, so there is little room for external customer revenue to grow much.

- AI (xAI): revenue of $3.2 billion, 17% of the total. And here lies the problem. This segment posted an operating loss of $6.4 billion in 2025 — and burned another $2.5 billion in Q1 2026 alone. In 2024, before the xAI merger, SpaceX was $790 million in the black. After the merger, the entire company flipped to a $4.9 billion loss. Put simply, xAI is eating the money Starlink brings in. Which leads to the central question. Price a company with $18.7 billion in revenue at $1.75 trillion and you get a P/S ratio of about 94x2. Nvidia, the most expensive company on Earth right now, trades at about 22x; Palantir, the highest-premium AI stock, at 67x; the S&P 500 average is 2.7x. 94x is higher than any large listed company today. Even Tesla never reached this level in its loss-making years.

Baked into that 94x is not just the business that exists today, but a heavy load of value from businesses that have not yet begun.

Optimism and Warning: Two Ways of Doing the Math

That SpaceX is not merely a rocket company is beyond dispute.

The core is the concept of orbital AI data centers. In space, solar energy is nearly unlimited and cooling costs nothing, eliminating the two biggest cost drivers of terrestrial data centers. Musk has long claimed that “within 2–3 years, orbit will be the lowest-cost venue for AI computing,” and in the June 10 webinar summarized by Samsung Securities, SpaceX’s COO stated that “by the end of next year, orbital computing will be cheaper than ground-based computing.”

SpaceX has already applied to the FCC for a license to operate 1 million satellites. Technical details disclosed in the same webinar: each Starship V3 can carry about 50 AI computing satellites, the company aims to expand to 5 launch pads within the year toward a target of 10,000 launches annually, and it is reportedly building a 10 million-square-foot solar cell production facility outside Austin, Texas.

Is there any company on Earth besides SpaceX that could make this real? It is the only firm that combines launch vehicles with large-scale satellite operations know-how — and that is the strongest pillar of the bull case. The $250 billion in institutional oversubscription is a bet on exactly this vision.

Morningstar analyst Nicolas Owens set SpaceX’s fair value at $63 per share, or a $780 billion company valuation. Less than half the IPO price.

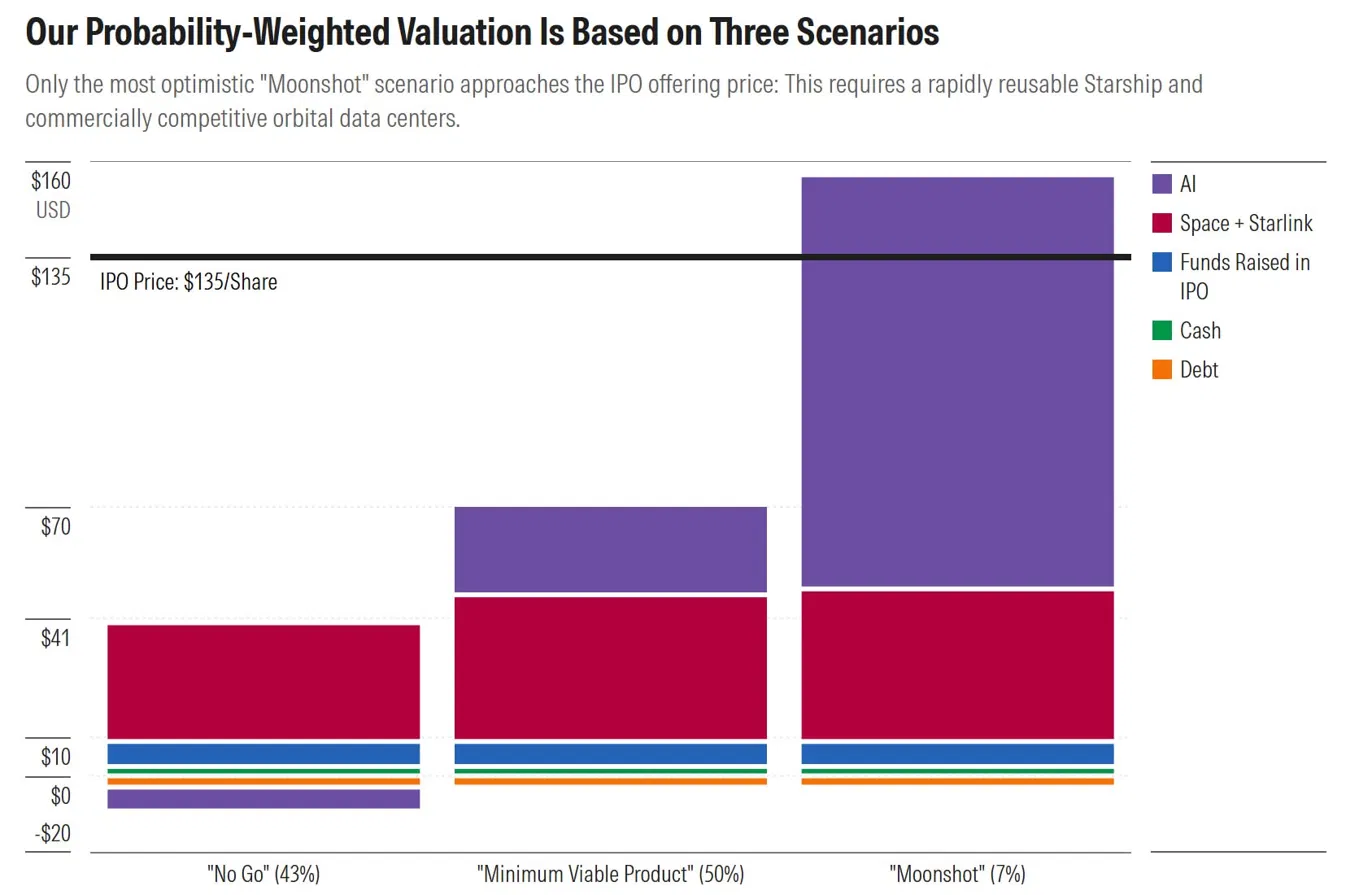

Morningstar’s method is interesting. It assigned probabilities to three future scenarios and took the weighted average.

- Moonshot scenario (probability 7%): Starship reusability is perfected, and the orbital AI platform captures 20% of global AI computing by 2040. Annual revenue of $225 billion, a $1.97 trillion valuation, $154 per share. It is the only scenario above the IPO price — by 14% — and Morningstar gives it just a 7% chance.

- Minimum-execution scenario (probability 50%): orbital data centers commercialize to a degree, but with capacity and latency constraints. About 4% of the AI computing market, annual revenue around $47 billion.

- Failure scenario (probability 43%): orbital data centers either don’t work technically or can’t beat terrestrial economics, and the project is shut down around 2028. Tens of billions of dollars of investment become sunk costs. Weight those three scenarios and you get $63 per share. And here is the decisive calculation. To justify the $135 IPO price, you must assume a 77% probability for the moonshot scenario, 23% for minimum execution, and effectively 0% for failure. In other words, investors are paying an extra ‘option premium’ of roughly $72 per share.

The gray-market futures are sending a signal too. Just before listing, SpaceX’s projected valuation in the unofficial pre-IPO market plunged by $300 billion (about ₩410 trillion). Expectations that once flirted with $2 trillion have settled down to $1.7–1.8 trillion — right around the IPO price. Whether that is speculative froth cooling off or realistic price discovery beginning is open to interpretation.

One more data point worth examining. Truist Securities recently analyzed the post-listing performance of 30 high-profile IPOs. Only 43% of them traded above their IPO price 6 and 12 months after listing. The median stock actually fell 9%, and the average maximum first-year drawdown was 55%. Meta (Facebook) once dropped 54%; Palantir, 53%. First-day excitement and the reality 1 year later are different games.

Oswarld’s Take

To be honest, when I look at this IPO, what I see first is not the ‘rocket’ but the ‘GTM strategy.’ There is a pattern I have seen countless times while designing market-entry strategies: cases where ‘the value of what hasn’t been built yet’ weighs more than the value of the existing business. Amazon was like that. So was Tesla.

But SpaceX has one distinct difference: the gap between present value and future value is historically unprecedented. By Morningstar’s math, the existing space + Starlink business is worth about $40 per share — roughly 30% of the IPO price. The remaining 70% is the value of ‘things that do not yet exist’: orbital AI data centers, semiconductor manufacturing on the Moon, cities on Mars.

What I am watching most closely is the demand architecture of this IPO. The 30% retail allocation, the 15-day Nasdaq-100 inclusion rule, and a micro-float with only 3% of total shares hitting the market. Combine the three and you get a structure where, right after listing, demand overflows while supply is severely constrained. Through a GTM lens, this is precisely the pattern of ‘locking in distribution channels and pent-up demand before the product launches.’

The problem is that this artificial supply-demand structure does not last forever. The timing of insider lock-up expirations, the burn rate of the IPO proceeds, and the first technical validation results from the orbital data centers — the real price will be set where those three variables meet. SpaceX’s technical capability is beyond doubt. The question is not the technology; it is the price tag hung on it.

Closing

On the eve of the biggest IPO in history, the market’s voices are split to the extremes.

Let me pull the threads together. Starlink is a proven business with 12 million subscribers generating $11.4 billion a year. But 70% of the $135 IPO price is a bet on orbital AI data centers — a future that has yet to put a single satellite up. Whether that bet is rational depends not on the technology, but on how you read the probabilities.

Soon, on June 12, when the Nasdaq opening bell rings, we get the first answer in that game of probabilities.

※ This newsletter is not investment advice recommending the purchase or sale of any specific security. Investment decisions are solely your own responsibility.

Do you see SpaceX’s $135 as the price of a dream, or the price of a bubble? Leave your thoughts in the comments.

References & Further Reading

Primary sources

- Nicolas Owens, “Why We Think the SpaceX IPO Is Overvalued”, Morningstar, 2026.6.8. : The original Morningstar analysis. The scenario-probability methodology is especially worth reading.

- “6 Charts on SpaceX’s Pre-IPO Financials”, Morningstar, 2026.5.20. : The S-1’s revenue, profit, and segment structure summarized in 6 charts. If you want the numbers at a glance, start here.

- Junkyu Park, “SpaceX Public Webinar Takeaways”, Samsung Securities Global Equity Team, 2026.6.10. : Covers the COO’s remarks and segment-by-segment Q&A. The orbital computing cost forecast is striking.

- “Projected SpaceX valuation falls by $300 billion in pre-IPO futures market”, WSJ, 2026.6.10. : Coverage of the gray-market futures plunge.

Background

- SpaceX S-1 Filing, SEC, 2026.5.20. : SpaceX’s financial statements and business plan in the original. The primary source for every figure.

- “SpaceX needs to grow at a rate no company has ever achieved to justify a $1.75 trillion valuation”, Fortune, 2026.6.6. : Calculates what growth rate would be required to justify the IPO price.

- “CIO Weekly: To Infinity and Beyond…SpaceX’s IPO”, Neuberger Berman, 2026.6.8. : A valuation frame from the institutional investor’s perspective. Its alternative angle — 25x EV/revenue on 2027 estimates — is intriguing.

Author Kwangseob Ahn is a professor of business administration at Sejong University and lead consultant at OBF (Oswarld Boutique Consulting Firm). At the university he teaches statistics and data analysis — business data management and business analytics — while in the field he leads GTM strategy and AI strategy consulting, designing the interface between technology and business. He has published academic research on memory architecture for AI dialogue systems (HEMA) and runs Daily Arxiv, a project curating global AI papers every day. He completed a master’s program at Korea University’s Graduate School of Management of Technology and its KMBA. He is the author of Those Who Outsource Their Thinking: Homo Brainless.

Footnotes

-

S-1 Filing: The IPO prospectus filed with the U.S. Securities and Exchange Commission (SEC). Because it is the first document to disclose a company’s financial statements, business model, and risk factors, it is sometimes called a ‘corporate X-ray.’ ↩

-

P/S Ratio (Price-to-Sales Ratio): Market capitalization divided by annual revenue. It shows how much investors pay for each unit of a company’s sales. At 94x, investors are paying $94 for every $1 of revenue. ↩